UK manufacturers are more optimistic about their business situation and exporting prospects, while reporting strong growth in domestic orders over the previous quarter, according to the latest quarterly CBI Industrial Trends Survey.

The survey of 461 manufacturers reveals that the volume of domestic orders rose at the fastest pace since July 2014 in the three months to January, while export orders continued to grow, but below expectations. Headcount edged higher having dipped for the first time in more than six years in the last quarter.

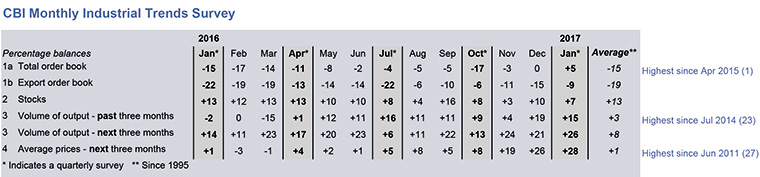

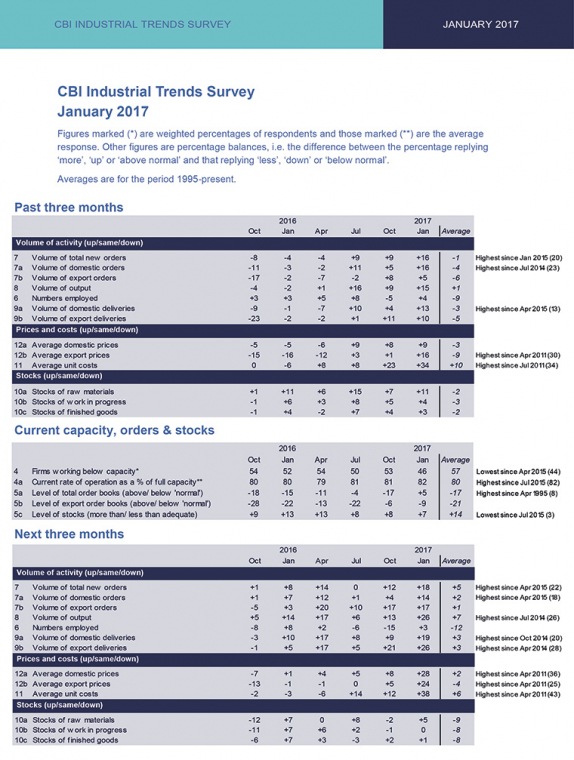

CBI Industrial Trends monthly results

Demand is expected to grow strongly over the next three months, driven by both domestic and export orders, while production is also expected to advance briskly – expectations for output growth are also the highest since July 2014.

Concerns persist over access to skilled labour, however, with almost a quarter of respondents – the highest since July 1989 – observing that skilled labour availability could limit output over the next few months.

Sterling’s depreciation continues to impact prices as unit costs rose at their highest pace in over five years, amid expectations that this will intensify over the next quarter. But on the flip side, manufacturers continue to see the competitive benefits arising from sterling’s weakness, reporting a further strong rise in competitiveness within the EU and putting the rise in competitiveness in non-EU markets at a survey high.

The pick-up in output has meanwhile eaten into spare capacity, pushing the proportion of firms citing capacity expansion as an investment driver to a survey high. Firms are planning to increase investment in product & process innovation and training & retraining over the year ahead at the fastest pace in two years, while investment plans for building and plant & machinery have moved back above their long-run averages.

Rain Newton-Smith, CBI chief economist

“UK manufacturers are firing on all cylinders right now with domestic orders up and optimism rising at the fastest pace in two years."

“The weaker Pound is driving export optimism for the year ahead, but is having a detrimental impact on costs for firms and ultimately for consumers. The new Industrial Strategy can support our manufacturing base by offering a shared long-term vision for the key sectors and regions of the economy and evidence-based plans for government and business collaboration. The CBI and its members across the country stand ready to support the Government in achieving this.”

Key findings – past quarter:

• Domestic orders rose at their fastest pace (+16%) since July 2014 (+23%). Export orders rose more moderately (+5%), and below expectations (+17%)

• 37% of businesses reported an increase in total orders, and 21% a decrease, giving a balance of +16%

• 32% of firms said the volume of output over the past three months was up and 18% said it was down, giving a balance of +15%

• 22% of manufacturers said employment numbers were up, and 18% said they were down, giving a balance of +4%

• 27% of firms said they were more optimistic about the general business situation than three months ago and 12% were less optimistic, giving a rounded balance of +15% – the highest since January 2015 (+15%). Optimism about export prospects for the year ahead rose strongly (+19%)

• Firms competitiveness in the EU rose strongly again (+28%) while their competitiveness in non-EU markets rose at the fastest pace in the survey’s history (+26%)

CBI Industrial Trends quarterly results

• Average domestic prices continued to grow at an above average pace (+9% vs -3%) for the third quarter in a row, while average export prices rose strongly (+16% vs LR average of -9%).

• The proportion of firms working below capacity (46%) was at its lowest since April 2015 (44%)

• Manufacturers intend to increase spending on product and process innovation strongly over the year (+27%) and a higher rate level than in the previous quarter, while spending on training and retraining also continued to grow robustly (+27%).

• The number of firms citing access to skilled labour as a factor likely to limit output (24%) was at its highest since July 1989 (24%).

Key findings – next quarter:

• Total new orders are expected to grow strongly (+18%), as are domestic orders, though at a slightly slower pace (+14%).

• A balance of +17% expect export orders to rise

• Expectations for output growth (+26%) are the strongest since July 2014 (+26%)

• Average domestic prices (+28%), export prices (+24%) and unit costs (+38%) are all expected to rise at their strongest rates since April 2011